Between online bill pay, debit cards and peer-to-peer payment apps, paper checks just aren’t as necessary as they used to be. But there still might be a few times when writing a check comes in handy, such as birthday gifts, business expenses or with older bill payment systems. Here are six simple steps to guide you on how to write a check correctly.

Step 1: Date the check

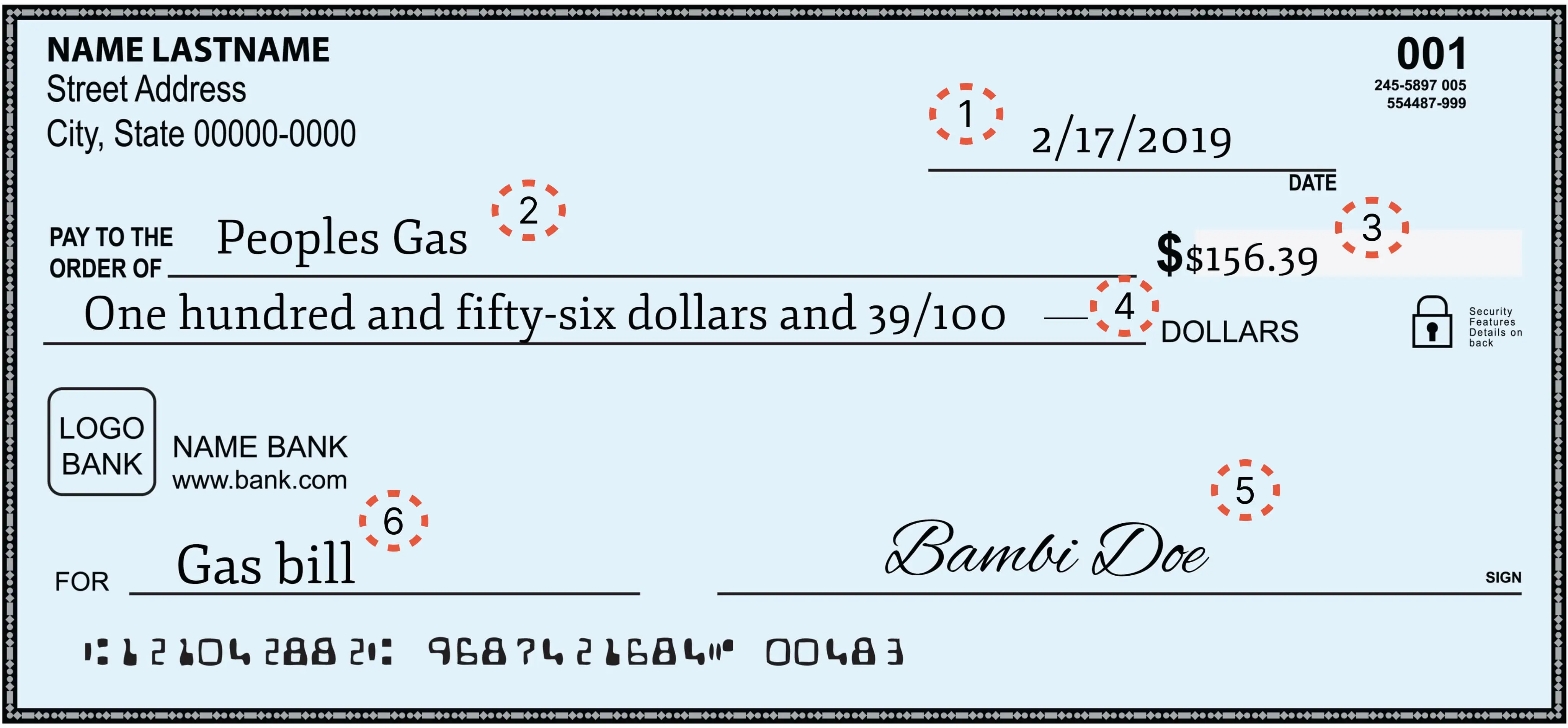

Write the date in the top right corner, next to a box or line that says “Date.” Always write the same date as when you signed the check.

Step 2: Write the recipient’s name

Write the recipient’s name on the line next to “Pay to the order of.” If it’s a person, write their first and last name. If it’s a company, make sure you have the correct company name for payments, only using acronyms if asked to. You can also write “cash” here, which means anyone can take the check to the bank and get the cash from your account.

Who is most likely to be researching how to write a check?

Finder data suggests that men aged 25-34 are most likely to be researching this topic.

Response

Male (%)

Female (%)

65+

2.38%

2.85%

55-64

4.49%

4.12%

45-54

7.48%

6.53%

35-44

11.34%

9.86%

25-34

15.56%

11.81%

18-24

12.36%

11.23%

Source: Finder sample of 4,320 visitors using demographics data from Google Analytics

Step 3: Write out the amount in numerals

Next to the dollar sign ($), write in numerals the amount of money the check is for, which will be the amount withdrawn from your account. Include the pennies, even if that amount is zero, for example, “$100.00“.

Step 4: Write out the amount in words

Next, spell out the dollar amount on the line under the recipient field, including the cents as a fraction. It’s a good idea to draw a line afterward so no one can add to your check. For example, “One hundred dollars and 00/100 cents ——“.

Step 5: Sign the check

The bottom right corner of the check has a space for your signature. If you don’t sign there, the check won’t be valid.

If you’re using a checkbook with duplicates, tear off the top check. The top copy is what you give your recipient. The second, lighter copy is called a carbon copy — it’s for you to keep. After you sign it and tear off the check, it’s ready to go.

Step 6: Optional, fill out the memo

You don’t have to do this, but it’s still a good idea. You can write in the Memo section of the check, which states what the check is for. It can help you keep track of your finances and let the recipient know what the check is intended for, such as “Birthday” or “Rent.”

If you wrote a check that you don’t want anyone to cash, there are three ways to void it. But you’ll want to act as quickly as possible because your bank can’t do anything once it’s cashed.

Write VOID across the check. If you still have the check in your possession and you wrote in the wrong information, write the word VOID across the check as clearly and as largely as you can, making sure it covers the entire check.

Void it online. Depending on your bank, you may be able to log in to your account and cancel the check. If not, look for a live chat function on your bank’s website where you can request a stop payment order with a customer service representative. Be prepared to give your account number, check number and the exact amount you wrote the check out for.

Void it by calling the bank. If you can’t or don’t want to cancel the check online, you can call your bank to request a stop payment order. You’ll need to give the representative your account number, check number and the exact amount of the check, so have this information on hand before you call.

If the bank has to authorize a stop payment request, you may pay a fee, which typically runs around $30.

How to write a check out to cash

The same steps apply as when you write a check out to someone, with one minor exception. Instead of writing the name of the recipient, you’ll write “Cash” in the “Pay to the order of” section.

Checks are safer than cash because only the recipient can cash the check. But when you write a check out to “Cash,” anyone can receive the funds — whether you want them to or not. For this reason, it’s usually not advisable to write a check out to cash.

Writing a check to yourself

If you want to move money from one account to another, you can write a check to yourself by writing your own name in the “Pay to the order of” field. You’ll also need to sign the back of the check before you deposit it.

When drawbacks outweigh the benefits

Checks come with a few notable drawbacks that leave them inconvenient choices for any purchase that doesn’t require one.

They cost money. Most banks require you to shell out some cash to receive a new allotment of checks from your bank.

They take longer to clear. Compared to credit or debit cards, checks take longer to clear with your bank. Most checks clear within two to three business days, though checks that look suspicious or come from an unfamiliar or overseas bank may take longer.

Less secure than other payment methods. Checks carry a lot of personal information on them, including your name, address, bank routing and account number that someone can steal.

Potential to expire. Banks don’t have to honor checks older than six months.

Do I have to write a check?

The short answer is no. There are likely very few instances where you’ll need to write a check. Most merchants and consumers have moved on to the numerous new methods of digital payments that have become available over the last few years.

4 alternatives to use instead

Here are some of the more popular alternatives to checkwriting, many of which are peer-to-peer (P2P) payment platforms that are free to download:

Zelle. Many bank accounts now feature Zelle integration, an app that allows easy bank transfers between two users. But keep in mind that Zelle is US only and lacks fraud protection.

Venmo. A popular P2P app for smart devices that’s free to download and use, Venmo offers a convenient way to send money to friends or family and offers a split-bill option. In addition, it offers a debit card, which lets you use your Venmo balance without dipping into your linked checking account. But it lacks an ironclad fraud protection program.

Cash App. Another popular P2P app for all phones,

Cash App offers a fast and easy way to send money to friends and family. Similar to Zelle and Venmo, it doesn’t have a great fraud protection program either. Other perks include its checking, savings and cash advances.

Bill pay. Most checking accounts have a “bill pay” feature that lets you set up automatic bill payments through your checking account‘s banking app without needing to write a check.

Bottom line

The easiest way to make payments or transfer money is online or via an app. But if you need to go old school, writing a check is simpler than it looks. And some banks will even print out a check for you at the teller if you don’t have a checkbook handy.

Bethany Hickey is the banking editor and personal finance expert at Finder, specializing in banking, lending, insurance, and crypto.

Bethany’s expertise in personal finance has garnered recognition from esteemed media outlets, such as Nasdaq, MSN, Yahoo Finance, GOBankingRates, SuperMoney, AOL and Newsweek. Her articles offer practical financial strategies to Americans, empowering them to make decisions that meet their financial goals. Her past work includes articles on generational spending and saving habits, lending, budgeting and managing debt.

Before joining Finder, she was a content manager where she wrote hundreds of articles and news pieces on auto financing and credit repair for CarsDirect, Auto Credit Express and The Car Connection, among others.

Bethany holds a BA in English from the University of Michigan-Flint, and was poetry editor for the university’s Qua Literary and Fine Arts Magazine. See full bio

Bethany's expertise

Bethany has written 424 Finder guides across topics including:

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Advertiser Disclosure

finder.com is an independent comparison platform and information service that aims to provide you with the tools you need to make better decisions. While we are independent, the offers that appear on this site are from companies from which finder.com receives compensation. We may receive compensation from our partners for placement of their products or services. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn't influence our assessment of those products. Please don't interpret the order in which products appear on our Site as any endorsement or recommendation from us. finder.com compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.